Read an interactive and user-friendly version of this guide below.

Updated in March 2026.

As a landlord with an investment property, you’re likely to pay tax at every stage of the life of that investment: when you buy the property, when you let the property, and later when you sell or pass it on.

In short, letting is like any other business: if you make a profit, it’s liable to taxation. However, property tax is a specialist area and navigating the rules can be complicated - particularly for new landlords.

Whatever money you make from property, do remember that the tax you pay will not be dictated to simply by your property earnings, it’s the total income and capital gains you make that determines your final tax bill.

That’s where this guide comes in. It outlines all the key things you need to know about the taxes landlords pay and covers some of the ways you can reduce your tax liability.

Of course, for personal, tailored advice, you should consult a tax professional – ideally one who’s experienced in buy to let taxation - who can help ensure you invest in a tax-efficient way that’s appropriate for your own circumstances.

Meanwhile, this overview should help you understand your liability so you can budget properly and make sure you don’t get any surprise demands from HMRC!

In this guide, we’ll cover the following topics:

Bear in mind, this guide is meant as a general overview of the current tax landscape. For further, more in-depth personal tax advice tailored to your specific requirements and circumstances, make sure you seek professional advice from a tax specialist.

Everyone in the UK pays tax when they buy a property over a certain price (commonly known as ‘stamp duty’), but if a property isn’t your primary residence and you let it out, you are also liable to taxation on:

Let’s take a look at those three types of taxation in more detail.

When you buy any residential property in the UK over a certain value, you have to pay a purchase tax. Although different parts of the UK have different systems, they all work in a similar way to income tax, with ‘bands’ set for various portions of the property value and the rate of taxation increasing with each band.

The key thing for landlords to know is that there’s then an additional rate that applies if you’re buying a residential property for more than £40,000 and you already own one (or more) – i.e. this additional rate applies to the full price you pay for buy to lets and second homes.

Here’s a summary of how the purchase tax is currently applied:

If you buy a home for yourself in England or Northern Ireland, you don’t pay any tax on the first £125,000 of the purchase price.

The higher zero-rate threshold of £250,000, which was in effect from 23 September 2022, dropped back to its former level of £125,000 from 1 April 2025.

However, if it’s a buy to let or second home worth more than £40,000, you pay an additional five per cent and it’s important to note that this applies to the whole amount – there is no ‘zero’ band for additional properties.

This rate was increased from five per cent in the 2024 Autumn Budget and came into force from midnight on 30 October.

.png)

See the government website for full details.

Example

If you were to buy an investment property for £300,000 in the 2025-25 tax year, the SDLT calculation would be:

The first £125,000 x five per cent £6,250

The next £125,000 x seven per cent £8,750

The final £50,000 x ten per cent £5,000

Total tax due: £20,000 (versus £5,000 if it were your own home, or zero for first time buyers)

You must send a SDLT return to HMRC and pay the tax due within 14 days of completing the purchase. Generally speaking, your solicitor or conveyancer will do this on your behalf and add the stamp duty charge to their total bill, but do check with them that they are doing the paperwork and paying it on your behalf.

Note: Although this additional rate is an extra ‘up-front’ cost for landlords, you can offset the entire amount of stamp duty against your capital gains when you come to sell or dispose of the property.

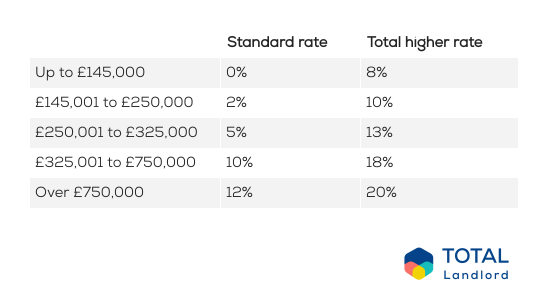

In Wales there is also a, the higher rate for investment properties and second homes. As in England, this additional rate applies to the whole purchase price if the property is worther £40,000 and all LTT due must be paid within 30 days of completion.

On 10 December 2024, the Welsh Government announced that the higher rate would be raised by 1%, effective from 11 December. The current rates are:

For full information, visit the Welsh Government website.

In Scotland, an Additional Dwelling Supplement is charged at eight per cent of the total purchase price. This was increased from six per cent in the Government’s 2025-26 Scottish Budget and applied to all contracts entered into from 5 December 2024.

The return must be lodged and payment made within 30 days of completion, which can be done via the Revenue Scotland online portal.

Full information on LBTT is available on the Scottish Government website.

If your annual rental profit is above £2,500 or your rental income before allowable expenses is greater than £10,000, you must complete a self assessment tax return. If you earned less than £2,500, you can check whether you need to complete a tax return using this online tool.

Your profits from property will then be added to any other earnings to give an overall personal income, on which you then pay income tax at the applicable rate.

The expenses you are and aren’t allowed to claim for are complex and are covered in the next section.

For the 2025/26 tax year in England and Wales, you’ll be taxed at 20% on earnings falling between the personal allowance of £12,570 and basic rate upper threshold of £50,270, and 40% on any amount between that and £125,14. Earnings over £125,240 will be taxed at 45%. and you do not get a personal allowance in this highest-rate band

These thresholds are currently* frozen until April 2028, they change, it’s likely to happen at a budget, so do check the government website for the latest updates.

(*If these thresholds change, it’s likely to happen at a budget, so do check the government website for latest updates.)

You may also have to pay National Insurance, but this can be quite a complex issue, so it’s best to speak to a professional to check your obligations. Class 4' NI contributions paid on self-employed profits of between £12,570 and £50,270, dropped from nine percent to six per cent cent from 6 April 2024.

In Scotland, the personal allowance is the same as in England and Wales, but the banding thereafter is more complex and has been revised for 2025-26.

.png)

*Assumes individuals are in receipt of the standard Personal Allowance.

**Those earning more than £100,000 will see their Personal Allowance reduced by £1 for every £2 earned over £100,000.

Even if you never directly receive the rental income from your property yourself – e.g. if you have a property manager who collects the rent and keeps it in return for their work – you need to declare it on your self assessment tax return, indicating where the money ends up.

This is to avoid tax mismatches and make sure that the person who benefits from owning a property pays the tax. Some higher-rate taxpayers will attempt to hide their income and reduce their tax bills by passing off someone else – often a basic rate taxpayer – as the person who benefits from the income.

Please be aware that misrepresenting your tax situation by hiding where the money goes is tax evasion and illegal.

To minimise your tax liability legally, consult a property tax specialist, who can help you structure your investments and earnings in the most appropriate and tax-efficient way.

If you are letting a room in your own property, you can earn up to £7,500 tax free per year under the ‘Rent a Room Scheme’. However, it is worth checking whether it’s better to use this system or deduct business letting expenses from the rent including insurance, maintenance, repairs (but not improvements) and utility bills, although there will be a private use restriction for general home expenses

You may also be subject to capital gains tax when you sell your home.

Visit the GOV.UK site for more information on renting a room

Many landlords have several properties. When this is the case, tax liabilities are considered much the same as when running any other business.

For self assessment, the important thing to note if you have different types of rental, is that income from furnished holiday lets should be reported as a separate figure, as it’s classed as a ‘trade’ and some different tax rules apply.

UK rental properties, rents and expenses should also be accounted for separately from any overseas rentals let on a long lease. Holiday homes outside the EEA fall into the overseas rental category.

If you’re completing a paper tax return, the deadline is 31 October each year. Online submissions can be made until midnight on 31 January for the previous year’s return.

For much more information on how to file your return and make payments, see our article, ‘Tax deadline on 31 January: what landlords need to know’.

You should already be aware that the Government intends to move everyone over to a new online-only tax filing system through its Making Tax Digital (MTD) plan.

The most recent update was made in January 2024 to the information that need to be provided – see the latest notes for reporting property income and profits on GOV.UK.

MTD requires individuals and businesses to submit quarterly returns and an annual finalisation statement to HMRC via MTD compatible software and it will apply to self-employed individuals and landlords with annual business or property income of

If your income is under £30,000, you will not be mandated to use the scheme until a review into how it can be shaped to meet the needs of smaller businesses has been completed.

If you own property jointly – for example as a married couple – then you can each earn up to the minimum threshold (including any other income) before you need to use MTD.

You can sign up voluntarily now, so it’s worth looking into exactly what’s required now and discussing it with a property tax expert so you can make sure you have the most appropriate software ahead of the requirement coming into force.

When you sell or transfer ownership of a residential property that’s not your own home, any increase in value over the time you’ve owned it is potentially liable to Capital Gains Tax (CGT).

It’s important to note that the ‘gain’ is defined as the difference between the purchase price and the sale price (or current market value) – it’s not the amount of equity you’re left with after the sale. So, if you’re considering remortgaging and increasing your borrowing, it’s advisable to leave enough equity in the property to at least cover any capital gains tax bill in case you need to sell.

Gains from 6 April 2025 onwards:

You’ll pay:

As with Income Tax, you have an annual personal tax-free allowance applied to capital gains. This is currently £3,000, having reduced from £12,300 since 2022/3.

You can also deduct the costs of buying, selling or improving your property from your gain. This includes:

It can be tricky to work out whether some works should be classed as ‘improvements’ or if they would be viewed more as general maintenance costs. So it’s advisable to work with a property tax specialist who can make sure you include all the deductions you’re entitled to and that you declare the correct level of gains.

When calculating CGT, gains from other assets (such as shares) are added to your total gains for the year, although different CGT rates may apply depending on the type of asset.

If you are a higher or additional rate tax payer, CGT is currently charged at 24%, reduced from 28% as of the 2025/6 tax year.

This should help those paying tax at the higher rate offset the reduction in the personal tax-free allowance over recent years. As a simplified example, if you had a £100,000 net gain:

If you pay Income Tax at the basic rate, the calculation is a little more complicated. Your taxable capital gains (less your personal allowance) will be added to your taxable income. If this total falls within the basic rate Income Tax band, you’ll pay 18% CGT. Any amount above the basic rate band is charged at 24%.

If you once lived in the property that you currently let, you’re entitled to Private Residence Relief. This essentially means you don’t pay CGT for the years you lived there yourself, plus the final nine months that you owned the property, even if it was let during that time.

The relief is calculated on a percentage basis, for example:

And if you shared the home with your tenants – i.e. you were a ‘live-in’ landlord – you may be able to claim up to £40,000 against capital gains.

These gains are, of course, subject to allowable deductions and the annual exempt amount.

Again, working out relief can be a complicated calculation, so it’s best to seek professional tax advice.

A separate CGT return must be submitted and payment for any tax owed must be paid within 60 days of completing the sale.

Businesses are taxed differently to individuals. Instead of income tax and capital gains tax, they pay corporation tax on trading profits, investment profits and gains from selling assets.

The rate of corporation tax currently stands at 25% for companies with profits above £250,000. Those with profits of £50,000 or less pay 19%, while profits between those two figures will be taxed at a graduated rate.

If you choose to let property via a limited company rather than as a private individual, you have to register for corporation tax, prepare and file a company tax return and either pay corporation tax or report that you have none to pay. You also have to file statutory accounts with Companies House, along with an annual Confirmation Statement.

If your allowable expenses come to more than your rental income during a year, this is considered a loss for tax purposes.

Any loss is carried forward to the next year and offset against available profits. This must be done each year - you can’t store up losses to use when it suits you, such as to avoid becoming liable for higher rate income tax.

In the 2023/24 tax year, your rental income is £15,000 and your allowable expenses come to £18,000, leading to a £3,000 loss for the year. You pay no tax.

In 2024/25, your rental income is still £15,000 and you manage to bring down your expenses to £13,000, giving you a £2,000 profit. The £3,000 loss from the previous tax year is deducted from that profit, meaning you carry forward a loss of £1,000 and pay no tax for a second year.

In 2025/26, your expenses drop to £11,000 and your rental income rises to £15,450, giving you a profit of £4,450. Deduct the loss of £1,000 brought forward from 2023/24 and you’re left with a taxable income of £3,450. You’re now liable to pay income tax.

As a landlord, you should claim property expenses. Every pound spent on an allowable property expense can be deducted from your profits, which reduces your tax liability.

That means one of the most important administrative tasks for landlords is recording everything you spend on your rental property and carefully filing every receipt for activities related to the business of letting, managing and maintaining it.

The good news is there are lots of apps and software that can help with this, even allowing you to capture your expenses by photographing the receipts.

Essentially, residential landlords can claim for the day-to-day costs of letting, managing and maintaining their properties.

The key thing to know is that any expenses you claim as an income tax deduction must have been incurred ‘wholly and exclusively’ for the purpose of running your rental property business. In technical terms, they must also be ‘revenue expenditure’, which means they’re incurred in order to earn income.

Expenses that are not classed as ‘revenue’ – such as extension or refurbishment that enhances a property’s value – are usually ‘capital’ expenses, which can be deducted from the capital gain when you eventually come to sell the property.

Revenue expenses include:

Some of these are straightforward, but some – especially business expenses and repairs – are more complex, which is why it’s highly advisable to engage a tax specialist to handle your tax returns. You may also want to have them handle your regular bookkeeping, especially if you have multiple rental properties.

If you have a holiday let, it’s important to know that from 6 April 2025, furnished holiday let (FHL) relief no longer applies. The previous system – which included being able to deduct the full cost of mortgage interest from rental income and paying CGT at a reduced rate of ten per cent - has been scrapped, bringing FHLs more into line with standard residential lets.

Some of the key changes from 6 April 2025:

See the government website for more information and speak to a tax adviser to make sure you understand what you can and can’t deduct from your profits, both this year and when the changes to relief come into force next year.

Here’s a closer look at some of the key expenses you can claim as a residential landlord:

You can think of these as ‘operational’ costs – the admin side of running your property business

The easiest way to account for working from home and travel with your own vehicle is to use HMRC’s ‘common sense’ approach which is explained here.

However, if you work from home but run your properties through a limited company, you can’t use simplified expenses. In that case, there are specific formulas for splitting your bills between personal and business use, which a tax adviser can help you understand.

If you choose not to use the simplified formula, it’s best to consult a tax adviser to make sure you get your business expenses claim right, as it can be fairly complicated.

Mortgage interest used to be an allowable expense, so landlords could simply deduct any buy to let mortgage interest payments from their rental income each year.

However, this allowance was gradually withdrawn between 2017and 2020. Now you simply receive a tax credit equal to 20% of whichever is the lower out of:

This 20% tax credit also applies to the interest on any other money you borrowed to fund activity related to your property business, e.g. credit to buying equipment for your rental or loans to pay for repairs.

Professional fees that relate to the day-to-day running of the business are allowed.

So, fees from accountants, solicitors and surveyors for services such as chasing bad debts, evicting tenants in rent arrears and keeping financial records are allowed. You can also deduct the full letting and management fees from a letting agent.

Costs related to buying, selling or planning applications for a property are not deductible from income – they will form part of your capital gains tax calculation when you sell the property.

It is possible that some purchase costs could be allowed, such as mortgage arrangement fees and mortgage broker fees – although these are subject to the same Section 24 rules and treatment as mortgage interest.

And if you speak to your legal company, ask if they can split their time between that spent on conveyancing and their time in financing, as this can aid your tax accountant when deducting costs.

This is where the ‘revenue’ versus ‘capital’ expense consideration comes into play.

To be classed as a ‘revenue’ expense that can be deducted from income, the repair or replacement must simply return the property to its previous condition. If it increases the value – e.g. if you add a room through conversion or extension, or replace a simple kitchen with a significantly higher-value one – then you’ll have to wait until you dispose of the property, at which point you can deduct the cost from your capital gains.

However, if you’re replacing an item with something that’s just a more modern alternative, that will usually be allowed as a revenue cost, even if it does improve the property’s value – such as replacing single-glazed windows with double glazing.

Top tip: If you’re having refurbishment work carried out that’s a mixture of capital and revenue items, ask your contractors to invoice separately for repairs and improvements. This is just one reason why it’s helpful if you employ contractors that are familiar with buy to let properties.

You can claim ‘replacement of domestic items’ relief for things like:

And you can also include the cost of disposal of old items and delivery of new ones.

If you’re letting out a fully furnished property, you can claim Replacement Domestic Item relief, which took the place of ‘wear and tear allowance’ from 2016. However, under this scheme, the initial cost of purchasing domestic items for a dwelling house isn’t a deductible revenue expense, so no relief is available for these costs.

You can deduct the cost of any training and educational materials, as long as you’re reinforcing existing skills and have the relevant receipts.

For example, if you bought a book about property tax for landlords or attended a seminar to learn more about how to attract the best tenants, then those would be allowable expenses. But the cost of going on a course to ‘become a property millionaire’ or even learning how to tile a bathroom will probably not be deductible.

Rent arrears are the most likely bad debt for a property business, but it’s important to understand that a debt doesn’t become ‘bad’ simply because someone owes the money - you must make some reasonable effort to recover the money.

In the case of a tenant owing rent, this means you must have launched court proceedings or passed the case to a debt collector.

Once it’s clear that the debt will not be recovered – for example, if the tenant declares bankruptcy or simply vanishes – then it’s considered to be ‘bad’, as long as you are using an accruals basis as opposed to cash.

If you have income from property or land, you’re eligible for a tax exemption of up to £1,000 a year. And as a self-employed individual, you’re also entitled to a separate 'trading allowance' of up to £1,000 a year.

However, if you claim the trading allowance, you can’t claim any business expenses. The allowance is there to benefit low-income businesses and chances are that, as a landlord, you will have a far greater level of annual expenses to account for.

Tax rules concerning married couples and those in a civil partnership are complicated but can enable individuals to reduce their tax bill in a legally sound way. If you have income from property or land, landlords may claim the £1,000 trading allowance instead of deducting expenses if their rental income is low. There are two allowances you may be eligible for, depending on your income:

Given the complex nature of these particular tax rules, it’s highly advisable to consult a tax professional, who can review your specific situation and give you tailored advice.

Meanwhile, here is a simple overview of three ways in which couples may be able to reduce their tax liability:

Marriage Allowance lets you transfer £1,260 of your personal allowance to your husband, wife or civil partner. It can benefit couples where one person is earning less than the personal allowance (currently £12,570) and the other person pays income tax at the basic rate (i.e. their income is between £12,571 and £50,270).

The person with the lowest income needs to apply for Marriage Allowance online. This can take up to two months to be processed and then the person with the higher income will get their new personal allowance when they send in their next self assessment tax return.

As it stands, the higher earner’s tax bill could be reduced by up to £252.

Even if the reduction in the lower-earning person’s tax-free allowance means a small part of their income is now taxable, you could still pay less tax overall as a couple.

If you’re not sure what your taxable income is, or you receive other income - such as dividends, savings or benefits from your job - you should call the Income Tax helpline.

If you’re both basic rate taxpayers, one option is to set up a business partnership. Business partners share the profits from the business, but each partner only pays tax on their share. So, splitting the rental profits from your property business may mean you can avoid one or both of you moving into a higher income tax band.

Although we’ve explained this in some detail below, it is a complicated area of tax and you shouldn’t go down this route without the advice of a professional tax expert.

As a couple, you earn £50,000 a year from rental income and each earn £25,000 from other paid work.

(The following is a simplified calculation.)

If the whole £50,000 goes to one person, their total earnings of £75,000 will be taxed as follows:

Meanwhile, the other person will pay £2,486 in tax on their earnings (£25,000-£12,570 x 20%), meaning you pay a total of £19,918.

However, if this rent is paid to a partnership and each partner has a 50% share, each will receive £25,000 in rental income. Now the tax calculation is based on a total income of £50,000 for each person:

By setting up as a partnership, you have reduced the tax your household pays by £4,946 – which is now in your pocket rather than with HMRC.

Some landlords choose to use a limited liability partnership (LLP), although professional advice should be taken as it is not suitable in all cases. This helps protect you financially in the event that your business struggles in the future.

You’ll need to decide on a business name and choose a ‘nominated partner’ who must register the partnership with HMRC and will be responsible for sending the tax return for the business.

Both partners must be registered with HMRC and must send their own self-assessment tax returns.

Bear in mind that this is a very broad overview of partnerships and you should consult a tax specialist as well as taking legal advice before moving ahead with any such plans.

If you are married and one of you earns less than the other, as long as you own the property individually – via tenants in common – you can reduce the tax liability between you.

For example, if the higher earner owns a 20% share of the property and the lower earner 80%, then the income and any capital gains can be split 20/80. However, you can’t just decide this between you, it has to be reflected in the property’s ownership. As this can be quite complicated, we advise you to contact a property tax professional to assess your percentage split.

Private limited companies are legally separate entities from the people who run them.

One financial advantage of owning and/or letting property through a private limited company is that you can take profits out of the company in such a way that you pay less tax.

You can pay yourself a salary within the basic rate of income tax and have your partner claim Marriage Allowance - or pay your partner a separate salary. You can then pay out further profits to people with a share in the company, in the form of dividends.

Shares can also be bought, sold and transferred if you want to bring more members of your family into the company and it can be an effective way of avoiding having to pay income tax at the higher rate.

The disadvantage is that it takes more work to set up a private limited company than a partnership and you have various legal responsibilities as a director of the company.

As with partnerships in the section above, you should consult a financial adviser or wealth manager to discuss whether setting up a limited company would be appropriate or worthwhile for you and your business. It’s not right for everyone and is not something that should be entered into without serious consideration.

As if buy to let tax wasn’t fiddly enough, the rules can also change fairly regularly, so it’s important that you have a way of making sure you stay on the right side of HMRC.

By far the best way to make sure you meet your tax obligations but don’t pay more than you need to, is to engage a professional property tax expert – ideally someone who already has buy to let clients or is a landlord themselves. They can give advice that’s tailored to your own circumstances and complete your tax return on your behalf.

Even if you use a professional to handle all your bookkeeping and tax affairs, the more you know about tax yourself, the more productive your conversations with tax and financial advisers will be.

One way you can gain a better understanding is by attending one of the NRLA’s tax training courses for landlords, which include ‘Saving Property Tax’, ‘Capital Gains Tax’ and ‘Inheritance Tax’.

And if you find you have not been paying all the tax you should, disclosing this to HMRC may reduce the penalty you have to pay. For more information, see the government’s Let Property Campaign.

If you choose to file your tax return yourself, GoSimpleTax, has an online tax calculator that could be helpful. It lets you select your different sources of income – breaking it down clearly into categories including ‘Employment’, ‘Property’, ‘Furnished Holiday Lettings’ and ‘Rent a room’ - and then takes you through each one, step by step.

This tool is officially recognised by HMRC and has handy tips throughout that could alert you to allowances and expenses you may have overlooked.

Of course, we will continue to keep our own information up to date, so please do keep referring back to this guide and follow us on Facebook, X and YouTube for all the latest property news.